Jun 13, 2025 •

R2P + SCT Inst is finally a user-friendly payment method par excellence. The payment arrives in seconds, can be automatically booked and assigned - and the entire dunning process becomes much more efficient.

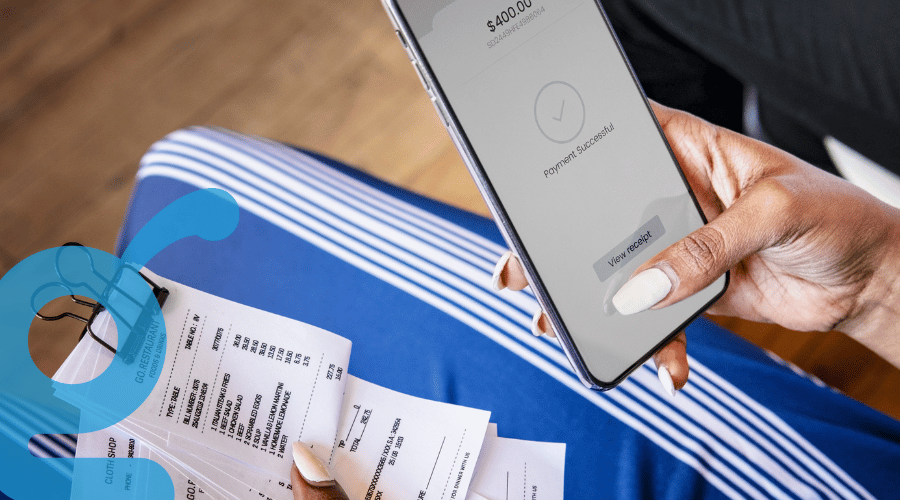

What if the payment of an invoice no longer failed because the invoice was sitting unnoticed in the mailbox, but the payment request landed directly in the banking app? And what if the transfer then arrived in the other account within seconds? The combination of SEPA Request-to-Pay (also known as R2P or SRTP) and SEPA Instant Credit Transfer (SCT Inst, Instant Payments for short) makes it possible. Let’s look at the opportunities this presents for the payments market.

From invoice to immediate payment – with a system

Instead of sending customers an invoice that they must pay manually, you send them a payment request. The payment request lands directly in the banking app via mobile banking. The customer can then decide to pay the invoice immediately or later within the payment period. The payment can then be initiated in no time at all – simply by clicking a button in the banking app—no need to manually type in the recipient details or enter the payment amount. The payment details are already filled out so that the payment can be made without problems. The reconciliation rate is therefore 100%. SEPA Request-to-Pay is consequently not only user-friendly but also offers high security when processing payments.

In combination with SCT Inst, the potential of SEPA Request-to-Pay increases significantly. After the payment request, the money can be received in seconds, and the payment can be completed in an instant.

From October 2025, SCT Inst will be mandatory for all banks in the eurozone. In concrete terms, this means that banks must enable their customers to receive and send payments within ten seconds—at the same cost as normal transfers—a development that will clearly benefit request-to-pay.

The two sides of a perfect payment

R2P + SCT Inst finally offers a user-friendly payment method par excellence. An invoice is no longer sent in isolation, but is actively embedded in a digital payment flow. For users, this means no more typing in IBANs or payment details, no more searching for the right payment method, and no more creating accounts with third-party providers. They can simply pay via the banking app without having to sacrifice a good UX or simple and secure handling.

At the same time, there is real added value for companies: the payment arrives in a matter of seconds, can be automatically booked and assigned, and the entire dunning process becomes significantly more efficient. Whether in B2C e-commerce, for suppliers, or in a B2B context, R2P + SCT Inst makes payment processes faster, more transparent, and more user-friendly. In the long term, payment methods such as SEPA direct debit will also be replaced by recurring payment requests with SRTP in a user-friendly way. And best of all, SRTP is significantly cheaper and just as fast as other payment methods. For banks, this offers the opportunity to become the preferred payment interface for users. New additional touchpoints lead to more engagement and traffic, which in turn opens up new revenue streams. In the long term, options such as SRTP will increase the use of the banking app and thus the value of users.

Why is now the right time for Request-to-Pay?

Request-to-pay is not a new concept, but the right environment for it is only now emerging. And there are several reasons for this:

1. Regulation provides a tailwind

The EU has set clear guidelines with the new Instant Payments Regulation: real-time transfers are becoming mandatory, but they must not be more expensive than traditional transfers. This removes one of the biggest hurdles to using SCT Inst.

2. The technical infrastructure is in place

With the increasing spread of open banking APIs, TIPS connections, and IBAN name checks, the technical foundations have been laid to implement SRTP in a secure and scalable manner.

3. The market is ready

More and more companies – from large suppliers to online stores – are looking for alternatives to expensive American payment methods, outdated invoicing processes, or the classic SEPA direct debit. At the same time, consumers are also expecting a modern, digital payment experience – ideally via the familiar banking app.

SEPA Request-to-Pay is not new. The concept of SRTP has been around for years, but now it is getting a boost from SCT Inst. Successful pioneers in Europe are impressively demonstrating how it works. In a particularly advanced market, the share of instant payments in the SEPA area is already over 50%.* The broad integration of almost all banks and a common clearing infrastructure has led to strong network coverage there, thus to real suitability for everyday use.

The effect: when infrastructure, regulation, and user-centricity come together, a case is created that not only makes SEPA Request-to-Pay technically possible but also economically viable and socially accepted.

This momentum is now beginning to spread across Europe: more banks are joining in, pilot projects are being initiated, and the first solutions are achieving real scaling. For R2P and SCT Inst, this means that now is the right time to set new standards in combination: more and more companies, from large suppliers to online stores, are looking for alternatives to expensive American payment methods, outdated invoicing processes, or the classic SEPA direct debit. At the same time, consumers are also expecting a modern, digital payment experience – ideally via the familiar banking app.

SEPA Request-to-Pay is not new. The concept of SRTP has been around for years, but now it is getting a boost from SCT Inst. Successful pioneers in Europe are impressively demonstrating how it works. In a particularly advanced market, the share of instant payments in the SEPA area is already over 50%.* The broad integration of almost all banks and a common clearing infrastructure has led to strong network coverage there, and thus to real suitability for everyday use.

The sweet spot for smart payments

The combination of SEPA Request-to-Pay and SCT Inst is more than just a technical upgrade. It changes how we pay – and how we as companies, banks, and users deal with payments. This is a huge opportunity for banks and FinTechs: if you want to offer your customers a smooth, secure, and transparent payment experience in the future, there is no way around this combination. At the same time, SRTP with instant payments will become a game-changer for companies in invoice processing.

*https://www.bde.es/wbe/en/noticias-eventos/blog/bizum-y-el-exito-de-las-transferencias-inmediatas-en-espana

At Gini, we want our posts, articles, guides, white papers and press releases to reach everyone. Therefore, we emphasize that both female, male, and other gender identities are explicitly addressed in them. All references to persons refer to all genders, even when the generic masculine is used in content.