May 13, 2025 •

Paying with a QR code enables fast and contactless payment processing. The method is becoming increasingly important in stationary retail, e-commerce and invoice payments.

Although paying with a QR code is a simple and efficient payment method, it is not yet widely used. It offers a high level of user-friendliness and is suitable for a wide range of applications.

The method is becoming increasingly crucial in stationary retail, e-commerce and invoice payments. After all, it enables fast and contactless processing – simply scan the QR code and pay. So it’s no wonder that more and more companies are integrating QR code payments into their systems to offer customers a flexible and secure payment option. But how exactly does the process work, what advantages does it offer and what future trends are emerging?

How does payment with a QR code work?

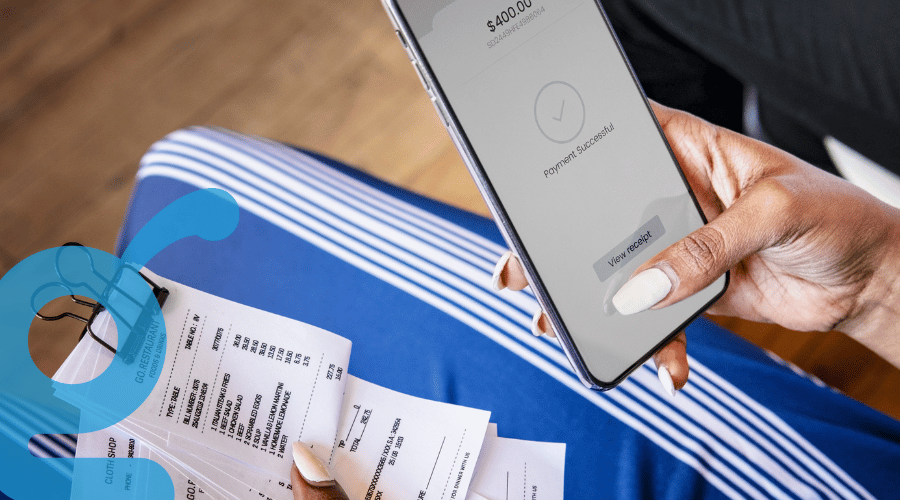

Paying with a QR code enables fast and contactless payment processing. The code contains all relevant payment information and is scanned by the customer using a smartphone. The process differs depending on the type of QR code – static or dynamic.

- Generation and display of the QR code: Merchants create static or dynamic QR codes. Static codes contain a fixed payment address, and customers must manually enter the amount. On the other hand, dynamic codes are tailored to a specific transaction and already contain all the payment details. For example, they are displayed on invoices, checkout displays, or online checkout pages.

- Scan and pay: Customers scan the QR code using a banking app. Alternatively, they can use their smartphone camera if it supports a direct payment option.

- Confirmation and processing: The payment details appear on the display after scanning. Customers can confirm the payment by PIN, Face ID or fingerprint. The transaction is then processed immediately. Merchants usually receive confirmation in real time.

The combination of speed, security and user-friendliness makes QR code payment an attractive alternative to conventional payment methods.

Advantages of QR code payments for companies and customers

The increasing popularity of QR code payments shows that they offer many advantages for companies and customers. In addition to ease of use and fast processing, cost efficiency and security also play a decisive role.

Efficient and cost-saving for companies

When payments are made by QR code, expensive card readers and additional hardware are no longer necessary. Companies benefit from a simple implementation that can be used flexibly in both stationary retail and e-commerce. The simple and fast handling significantly improves the customer experience. In addition, direct payment processing minimizes the risk of chargebacks or failed transactions.

Fast, secure, and convenient for customers

For consumers, paying with a QR code is a fast, contactless, and convenient solution. A simple scan with a banking app is all it takes to authorize the payment – without the need for a card or cash. The method also impresses with its high security standards. As no sensitive card data is passed on, the risk of fraud is reduced.

Paying with a QR code: How companies can integrate it

Implementing mobile payments using a QR code is flexible and can be adapted to different business models. Companies can either use existing solutions or generate their own QR codes to integrate the payment method into their systems seamlessly.

- Use of existing payment providers: Platforms like PayPal, SumUp or GiroCode offer ready-made solutions. Companies can generate individual codes linked to their business account – often without additional hardware or complex adjustments.

- Use of specialized solutions: Providers such as Gini enable a direct connection to German banking apps. Thanks to Gini QR Code Payment, invoices can be provided with a QR code that customers can scan with their banking app. The advantage is that payment data is automatically transferred so that customers do not manually enter an IBAN or payment reference. This speeds up the payment process and reduces errors.

Integration into existing systems occurs via POS systems, online stores or payment gateways. Many modern POS systems support QR code payments, while e-commerce platforms offer special plugins or APIs. These flexible implementation options benefit companies from efficient, secure and customer-friendly payment processing.

Comparison of providers for QR code payments

QR code payments are supported by various providers that differ in functionality, target group and area of application. While some solutions offer quick implementation for merchants, others are designed explicitly for SEPA transfers or optimized invoice payments.

- PayPal QR code payments: PayPal allows merchants to generate QR codes directly from their account. Customers can use these both in-store and online. The implementation benefits businesses already using PayPal as no additional hardware is required. In addition, payments are processed directly with the PayPal balance or a linked payment method.

- SumUp: This solution is aimed specifically at small businesses and the self-employed looking for an uncomplicated alternative to traditional card payments. Merchants can enter an amount in the SumUp app, generate a QR code and have it scanned by the customer to complete the payment. Additional hardware or a comprehensive POS system are not required, making the solution particularly cost-efficient.

- GiroCode for SEPA credit transfers: GiroCode is a cross-bank solution for SEPA credit transfers, which are primarily used for bill payments. Provided with a standardized QR code, customers can conveniently pay bills using their cell phones. They scan the code with their banking app, and the payment data is automatically transferred to the transfer form. This reduces input errors and speeds up the payment process.

- Gini QR code transfer: Gini offers an extended solution for paying bills with a QR code. Thanks to a seamless e-banking connection, the payment process is even more convenient and error-free for customers. In contrast to GiroCode, Gini enables intelligent data processing that automatically recognizes invoice details and transfers them correctly to the transfer form.

Choosing the right provider for QR code payments depends on individual requirements. PayPal and SumUp offer simple solutions for retailers and small businesses. GiroCode is suitable for standardized SEPA transfers, while Gini provides an optimized version with automatic data recognition.

Security and data protection when paying with QR code

As the QR code payment is based on the classic SEPA credit transfer, end-to-end encryption protects the data transfer, while two-factor authentication (e.g. PIN, Face ID or fingerprint) prevents unauthorized access. In addition, no sensitive bank or credit card data is stored directly in the QR code. This minimizes the risk of data misuse.

What are the risks?

Despite security measures, QR codes can pose a risk. Fraudsters paste over or replace genuine codes to redirect payments or lead users to phishing sites, a practice known as quashing. Caution is advised, especially in publicly accessible areas or on dubious websites.

How can retailers and customers protect themselves?

Careful handling when paying with QR codes helps to avoid fraud:

- Merchants: They should only use verified payment providers and generate QR codes directly from their POS systems or banking software. It is worth paying attention to corresponding data protection and cloud certifications.

- Customers: Consumers should only scan QR codes from trustworthy sources and carefully check the payment information displayed before confirming it.It is worth obtaining additional information about the merchants here; many payment service providers carry out additional checks on merchants.

The combination of technical protection mechanisms and a conscious approach means that paying with an online QR code remains a secure and reliable payment method.

Outlook for the future: QR code payments and new developments

QR code payments are gaining in importance worldwide – especially in retail and e-commerce. More and more companies are integrating this method as it offers a fast, secure and flexible alternative to traditional payment methods. The link to digital wallets such as Apple Pay and Google Pay increases user convenience and makes the payment process even more seamless.

Future developments could further improve the efficiency and security of QR code payments. NFC-QR hybrid systems could make contactless payments even more intuitive, while blockchain-based solutions create more transparency and security. At the same time, AI-supported security mechanisms could help to detect fraud at an early stage and secure transactions.

Government initiatives to promote cashless payments are also likely to accelerate the spread of QR code payments, which are increasingly becoming an integral part of modern payment transactions.

In addition, SCT Inst, i.e. instant payments, is ensuring that payment by QR code in e-commerce is becoming a strong alternative to PayPal and the like in Germany.

Paying with a QR code: A future-proof payment method

QR code payments offer a fast, secure and flexible alternative to traditional payment methods. They are easy to integrate, reduce transaction costs and improve the user experience. Companies benefit from uncomplicated implementation, while customers are impressed by the high level of security and ease of use.

Technological innovations such as NFC-QR hybrid systems or blockchain payments could further develop the method. As QR code payments become more widespread in retail, e-commerce and accounting, they will become a permanent fixture in digital payment transactions in the long term.

At Gini, we want our posts, articles, guides, white papers and press releases to reach everyone. Therefore, we emphasize that both female, male, and other gender identities are explicitly addressed in them. All references to persons refer to all genders, even when the generic masculine is used in content.